US Gold Card Visa Tax Implications: What Applicants Must Know Before Applying

Why Tax Planning Matters Before You Apply

For high-net-worth individuals considering the US Gold Card Visa program, the gift payment requirement ($1 million for the individual Gold Card plus a $15,000 processing fee, $2 million for Corporate, or $5 million for the Platinum Card which is not yet available pending Congressional approval) is only the beginning of the financial conversation. What many prospective applicants overlook is the profound and far-reaching tax transformation that accompanies US permanent residency. Unlike many other countries that offer residency-by-investment pathways, the United States operates one of the most comprehensive and aggressive tax systems in the world, one that reaches across borders and touches virtually every aspect of your global financial life.

The moment you become a US permanent resident through the Gold Card, you step into a tax framework that treats you almost identically to a US citizen for income tax purposes. This means your worldwide income, regardless of where it is earned, where it is held, or what currency it is denominated in, becomes subject to US federal income tax. For applicants who have structured their affairs around the tax regimes of their home countries, this shift can result in unexpected liabilities, penalties, and a fundamental disruption of long-standing wealth preservation strategies.

Gold Card holders ($1M individual gift payment) ARE US tax residents and are subject to worldwide income taxation, just like any other green card holder. The Platinum Card ($5M, not yet available pending Congressional approval) is the tier that has been discussed as potentially offering a special tax benefit — specifically, no US tax on non-US-sourced income. Do not confuse these two tiers. If you hold a Gold Card, you will be taxed on your worldwide income. The Platinum Card tax benefit is not yet available and would require Congressional approval to implement.

Proactive tax planning is not optional for Gold Card Visa applicants. It is an essential component of the application process itself. Applicants who begin their tax planning after obtaining residency often discover that they have missed critical windows for restructuring, have triggered unnecessary tax events, or have inadvertently exposed themselves to double taxation. The time to engage qualified international tax professionals is well before you submit any application, ideally twelve to twenty-four months in advance.

This article provides a broad overview of the tax considerations that Gold Card Visa applicants should be aware of. It is not a substitute for personalized advice from qualified tax and legal professionals who understand your specific circumstances, jurisdiction, and financial structure.

US Tax Residency — What Changes When You Get a Green Card

Obtaining permanent residency through the Gold Card Visa program fundamentally changes your relationship with the US tax system. Understanding the scope of these changes is the first step toward effective planning.

Worldwide Income Taxation

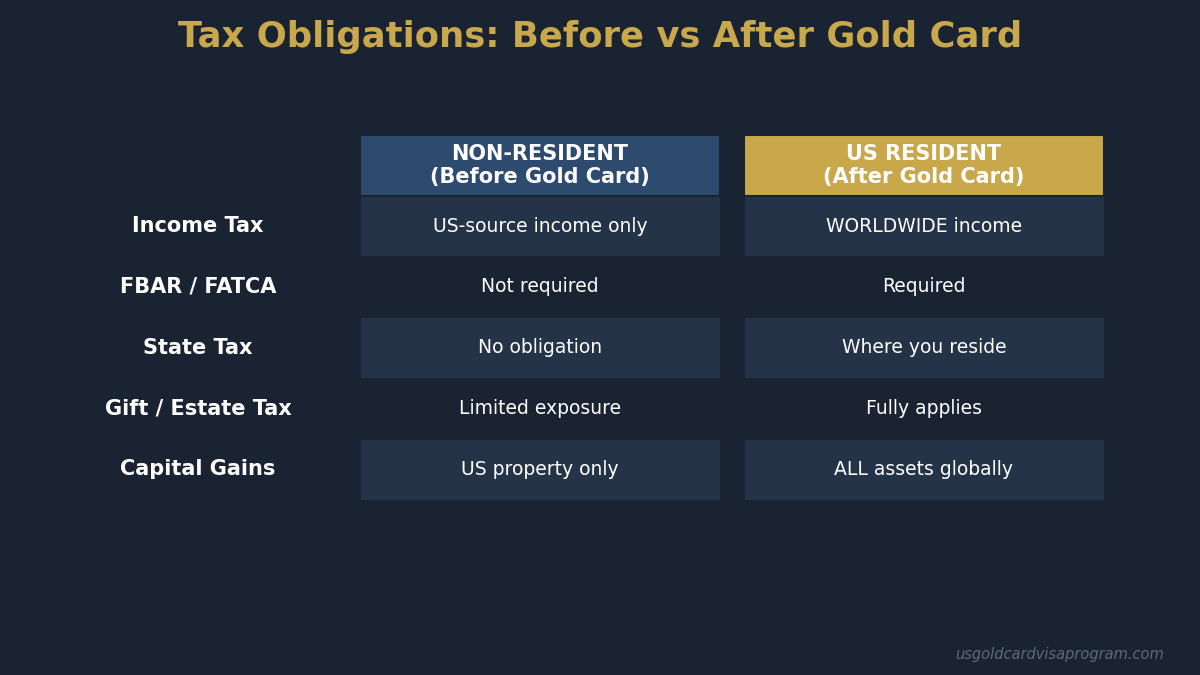

The United States taxes its residents and citizens on their worldwide income. Gold Card holders are US tax residents and are fully subject to this worldwide taxation. (The Platinum Card, at $5 million and not yet available, has been discussed as potentially exempting holders from US tax on non-US-sourced income, but this benefit does not apply to Gold Card holders.) As a Gold Card permanent resident, you will be required to report and potentially pay US federal income tax on all income from all sources globally. This includes salary and business income earned abroad, rental income from foreign properties, interest and dividends from foreign bank accounts and investments, capital gains on the sale of foreign assets, pension and retirement income from overseas plans, and income from trusts and partnerships established outside the United States.

While the US has tax treaties with many countries and offers foreign tax credits to help mitigate double taxation, these mechanisms do not eliminate the reporting burden, and they may not fully offset your US tax liability in every situation. The interplay between US tax obligations and the tax rules of your home country requires careful analysis by professionals with cross-border expertise.

FATCA Reporting Requirements

The Foreign Account Tax Compliance Act, commonly known as FATCA, imposes significant reporting obligations on US tax residents who hold financial assets outside the United States. If your specified foreign financial assets exceed certain thresholds, currently $200,000 on the last day of the tax year or $300,000 at any point during the year for individuals filing as single (higher thresholds apply for married couples filing jointly), you must file Form 8938 with your annual tax return. FATCA also requires foreign financial institutions to report information about accounts held by US persons directly to the IRS. This means that even if you fail to report, there is a high probability that the IRS will independently learn about your foreign accounts. For high-net-worth individuals entering the Gold Card Visa program, FATCA compliance is virtually guaranteed to be relevant, and the penalties for non-compliance are severe.

FBAR Reporting Obligations

Separately from FATCA, US tax residents must also comply with the Report of Foreign Bank and Financial Accounts, known as the FBAR or FinCEN Form 114. If the aggregate value of all your foreign financial accounts exceeds $10,000 at any point during the calendar year, you must file an FBAR. This includes bank accounts, brokerage accounts, mutual funds, and certain other financial accounts held outside the United States. The FBAR is filed separately from your tax return, directly with the Financial Crimes Enforcement Network. Penalties for willful failure to file an FBAR can reach $100,000 or 50% of the account balance per violation, whichever is greater. Even non-willful violations can carry penalties of up to $10,000 per account per year. For Gold Card Visa holders with substantial international assets, meticulous FBAR compliance is essential from the very first year of residency.

CRS and Information Exchange Implications

The Common Reporting Standard, or CRS, is an international framework for the automatic exchange of financial account information between participating jurisdictions. While the United States is not a CRS participant (it uses FATCA instead), many of the countries from which Gold Card Visa applicants originate are CRS signatories. This creates a complex web of information sharing that applicants must understand. Your home country may receive information about your US-based accounts through bilateral agreements, and conversely, the US may receive information about your foreign accounts through FATCA’s intergovernmental agreements. The practical effect is that financial transparency between jurisdictions is now the norm rather than the exception. Strategies that rely on information asymmetry between tax authorities are no longer viable and can expose you to severe legal consequences.

Free Gold Card Visa Guide

Get our Gold Card guide with cost breakdowns, timelines, and attorney tips. Delivered instantly to your inbox.

No spam. Unsubscribe anytime.

The Gold Card Gift Payment — Tax Treatment and Deductibility

One of the most common questions prospective Gold Card Visa applicants ask is whether the Gold Card gift payment ($1 million for the individual Gold Card, plus a $15,000 processing fee) carries any tax benefits. Understanding the tax treatment of this payment — which is structured as a gift to the Department of Commerce, paid after the vetting process is complete — is critical for financial planning purposes.

Non-Refundable Nature of the Fee

The gift payment required for the Gold Card Visa program — $1 million for the individual Gold Card plus $15,000 processing fee, $2 million for the Corporate tier, or $5 million for the Platinum tier (not yet available) — is structured as a non-refundable gift paid to the Department of Commerce after the applicant has been vetted. Unlike the EB-5 program, where the investment is placed into a qualifying enterprise with the expectation of return, the Gold Card gift payment is a direct, non-recoverable expenditure. This distinction has significant tax implications. Because the payment is a gift to a government department rather than an investment, it does not generate the types of tax attributes that investments typically produce, such as basis in an asset, depreciation deductions, or the potential for capital loss treatment.

Not Tax-Deductible

Based on the structure of the program as currently understood, the Gold Card gift payment is unlikely to be tax-deductible for US federal income tax purposes. It does not qualify as a business expense under Section 162 of the Internal Revenue Code, as it is a personal expenditure related to immigration status rather than a cost incurred in carrying on a trade or business. It is similarly unlikely to qualify as an investment expense, a charitable contribution, or any other category of deductible expenditure under current US tax law. Prospective applicants should plan on the assumption that the full Gold Card payment is a non-deductible, after-tax cost of obtaining permanent residency.

No Investment Loss Treatment

Because the Gold Card gift payment is not an investment in property or a capital asset, it is not expected to give rise to any capital loss deduction if the applicant later abandons their permanent residency or if the program undergoes changes. Unlike a failed business investment, where you might claim a capital loss or an ordinary loss under certain circumstances, a non-refundable gift to a government department generally does not create a tax-deductible loss. This is an important consideration when comparing the Gold Card Visa to other immigration pathways. The true cost analysis of the Gold Card Visa must account for the fact that the Gold Card gift payment produces no tax offset, recovery, or return. Applicants should work with their tax advisors to understand the full after-tax cost in the context of their overall financial plan.

Pre-Immigration Tax Planning Strategies

The period before you become a US tax resident is the most valuable window for tax planning. Once you hold a green card, many planning opportunities are permanently closed. The following strategies represent broad categories that qualified professionals may explore with you, depending on your specific circumstances.

Step-Up in Basis

One of the most powerful pre-immigration tax planning tools involves the concept of a step-up in basis. When a non-resident alien becomes a US tax resident, certain appreciated assets may receive a new cost basis equal to their fair market value on the date residency begins. This effectively eliminates the built-in capital gain that accumulated before US residency, meaning you would only be taxed on appreciation that occurs after you become a US tax resident. However, the rules governing step-up in basis are nuanced and do not apply uniformly to all asset types. Certain assets, such as interests in controlled foreign corporations or passive foreign investment companies, have special rules that may override the general step-up principle. Proper valuation and documentation of your assets before establishing residency is essential to support any basis step-up claims. Work with a qualified appraiser and tax professional to ensure that all valuations are defensible and properly recorded.

Trust Restructuring

If you hold assets through trusts, the transition to US tax residency requires careful analysis and potential restructuring. The US tax treatment of foreign trusts is extraordinarily complex, with specific rules governing grantor trusts, non-grantor trusts, trust distributions, and the classification of trust income. A trust that is tax-efficient in your home country may become a significant tax liability under US rules. For example, accumulation distributions from foreign non-grantor trusts can be subject to a punitive throwback tax that effectively imposes interest charges on deferred distributions. Pre-immigration restructuring might involve dissolving certain trusts, converting foreign trusts to US domestic trusts, making distributions before residency begins, or re-evaluating the terms and governance of existing trust structures. Each option carries its own implications, and the right approach depends entirely on your specific situation. The key point is that trust restructuring must happen before you become a US tax resident. Once residency is established, the options narrow considerably and the costs increase.

Exit Tax from Your Current Country

Many countries impose an exit tax or deemed disposition on residents who emigrate. Countries such as Canada, Australia, South Africa, and several European nations treat certain assets as having been sold at fair market value when you cease to be a tax resident, triggering capital gains tax on unrealized appreciation. If you are moving to the United States under the Gold Card Visa program, you must account for the exit tax obligations in your home country as part of your overall cost analysis. In some cases, treaties between your home country and the United States may provide relief from double taxation, but this is not guaranteed and varies significantly by jurisdiction. The timing of your departure from your home country relative to the establishment of US residency can also affect your exit tax liability. Working with tax professionals in both your home country and the United States is essential to minimize the combined tax burden of the transition.

Timing of Residency

The date on which you become a US tax resident has significant consequences for your tax obligations in the first year. Under US tax law, a lawful permanent resident is generally treated as a US tax resident from the first day they are physically present in the United States with their green card. Careful timing of your entry can minimize your US tax exposure in the transition year. For example, entering the United States later in the calendar year reduces the portion of the year during which your worldwide income is subject to US taxation. Similarly, the timing of significant financial events, such as the sale of appreciated assets, the receipt of large bonuses, or the distribution of trust income, should be coordinated with the establishment of your residency to minimize the overall tax impact. These timing decisions require detailed modeling by your tax advisory team, taking into account the tax rules of both the United States and your home country.

Ongoing US Tax Obligations for Gold Card Holders

Once you become a US permanent resident through the Gold Card Visa program, you will face ongoing tax obligations that extend well beyond the annual income tax return. Understanding the full scope of these obligations is essential for maintaining compliance and avoiding costly penalties.

Federal Income Tax

As a US permanent resident, you will file a US federal income tax return annually, reporting your worldwide income. The United States uses a progressive tax system with rates that currently range up to 37% for ordinary income at the highest bracket. Capital gains on assets held for more than one year are taxed at preferential rates of 0%, 15%, or 20%, depending on your total taxable income. Additionally, a 3.8% net investment income tax may apply to investment income above certain thresholds. For high-net-worth individuals entering through the Gold Card Visa program, it is reasonable to expect that you will be subject to the highest marginal rates. Your tax return will also need to include numerous information returns and disclosures related to foreign assets, accounts, entities, and trusts, as discussed throughout this article.

Estate and Gift Tax

The US estate and gift tax system is another area that requires immediate attention from Gold Card Visa holders. US residents and citizens are subject to estate tax on their worldwide assets at rates up to 40%. The current estate tax exemption is approximately $13.6 million per individual, but this exemption is scheduled to be reduced significantly in coming years unless Congress acts to extend it. For many Gold Card Visa applicants, whose net worth substantially exceeds these thresholds, estate tax planning is a critical concern from day one of residency. Gift tax rules also apply to transfers made during your lifetime. While annual exclusions allow for tax-free gifts up to certain amounts, larger transfers count against your lifetime exemption. Gifts to non-US-citizen spouses are subject to a separate and lower annual exclusion, which can create planning complications for Gold Card holders whose spouses have not also obtained US residency. Comprehensive estate and wealth preservation planning should be implemented promptly upon establishing residency.

State Tax Considerations

In addition to federal taxes, your choice of state of residence within the United States will significantly impact your overall tax burden. States such as California and New York impose income taxes at rates exceeding 13% and 10% respectively, while states such as Florida, Texas, Nevada, and Wyoming have no state income tax. For a Gold Card Visa holder with substantial income, the difference between residing in a high-tax state and a no-income-tax state can amount to millions of dollars over time. State estate taxes add another layer of complexity. Several states impose their own estate taxes with exemption thresholds much lower than the federal exemption, meaning you could face state estate tax even if your estate falls below the federal threshold. Your choice of state residency should be made in consultation with your tax advisory team and factored into your overall financial plan from the outset.

Common Tax Mistakes International Applicants Make

Even sophisticated international applicants can make costly tax mistakes when transitioning to US residency. Being aware of the most common pitfalls can help you avoid them.

Failing to Declare Foreign Accounts and Assets

The single most common and most dangerous mistake new US residents make is failing to fully declare their foreign financial accounts and assets. Whether through ignorance of the requirements, misunderstanding of what must be reported, or a misguided belief that foreign accounts are not visible to the IRS, the failure to file required forms such as the FBAR, Form 8938, Form 5471 (for controlled foreign corporations), Form 8865 (for foreign partnerships), and Form 3520 (for foreign trusts) can result in devastating penalties. The IRS imposes penalties of $10,000 or more per form per year for many of these information returns, even if no tax is owed. In cases of willful non-compliance, criminal prosecution is possible. The US government has invested heavily in international tax enforcement, and the era of undisclosed foreign accounts is definitively over. Full transparency and complete compliance from the beginning of your residency is the only viable approach.

Ignoring Exit Tax Obligations

Many investors become so focused on the US side of the equation that they neglect the tax consequences of departing their home country. As discussed earlier, numerous countries impose exit taxes or deemed dispositions that can trigger substantial tax liabilities. Failing to properly plan for and discharge these obligations can result in penalties, interest, and even legal complications in your home country. In some cases, unresolved tax obligations in your home country can affect your ability to access assets held there or create complications with future travel and business operations. A comprehensive transition plan must address the tax implications on both sides of the move.

Not Restructuring Before Arrival

Perhaps the most costly mistake of all is failing to restructure your financial affairs before becoming a US tax resident. Once you hold a green card, certain transactions that would have been tax-free or tax-efficient become taxable or trigger adverse consequences. Transferring assets to family members, restructuring trust arrangements, dissolving or reorganizing foreign corporations, and realizing capital gains on appreciated assets all have fundamentally different tax consequences depending on whether they occur before or after you become a US tax resident. The pre-immigration window is finite and irreplaceable. Investors who rush into the Gold Card Visa process without first completing their tax restructuring often face years of elevated tax burdens that could have been avoided with proper planning. This is why the recommended application timeline includes a substantial pre-application period dedicated to financial and tax preparation.

Overlooking Passive Foreign Investment Company Rules

International applicants often hold interests in foreign mutual funds, pooled investment vehicles, foreign corporations, and cryptocurrency holdings that qualify as Passive Foreign Investment Companies, or PFICs, under US tax law. The US tax treatment of PFICs is punitive by design, intended to discourage US persons from holding these types of investments. Income from PFICs can be taxed at the highest ordinary income rate plus an interest charge, even if the underlying income would otherwise qualify for lower capital gains rates. Many new US residents are shocked to discover that their existing foreign investment portfolios trigger PFIC treatment. Pre-immigration planning should include a thorough review of all investment holdings to identify PFICs and, where appropriate, restructure or liquidate these positions before residency begins.

Building Your Tax Advisory Team

Given the complexity of the tax issues facing Gold Card Visa applicants, assembling the right advisory team — starting with choosing the right immigration attorney — is not a luxury but a necessity. The cost of professional advice is invariably a fraction of the cost of the mistakes it prevents.

International Tax Attorney

An international tax attorney serves as the cornerstone of your advisory team. This professional should have deep expertise in US international tax law, including the taxation of foreign trusts, controlled foreign corporations, passive foreign investment companies, and cross-border transactions. Ideally, your tax attorney should also have familiarity with the tax system of your home country or work in collaboration with local counsel who does. The attorney-client privilege that applies to communications with your tax attorney provides an important layer of protection that is not available with other advisors. Look for an attorney with experience representing high-net-worth individuals in international tax planning, IRS compliance, and cross-border structuring.

CPA with Cross-Border Experience

Your Certified Public Accountant, or CPA, will handle the preparation and filing of your US tax returns and the numerous information returns required of international taxpayers. Not all CPAs are equipped to handle the complexity of international tax compliance. You need a CPA or accounting firm with specific experience in preparing returns for individuals with significant foreign assets, foreign trusts, foreign corporations, and multi-jurisdictional income sources. The CPA should work closely with your tax attorney to ensure that the planning strategies developed by the attorney are properly reflected in your tax filings. In many cases, the best approach is to work with a large accounting firm that has international tax specialists and offices in multiple jurisdictions, though specialized boutique firms can also provide excellent service.

Wealth Advisor with International Expertise

Your wealth advisor or financial planner coordinates the broader financial picture, ensuring that tax planning is integrated with your investment strategy, estate plan, risk management approach, and long-term wealth preservation goals. For Gold Card Visa applicants, the wealth advisor should have experience with international clients, understand the implications of US tax residency on investment portfolio construction, and be able to coordinate effectively with your tax attorney and CPA. The wealth advisor plays a particularly important role in restructuring investment portfolios to eliminate PFIC exposure, optimizing asset location between US and foreign accounts, and implementing estate planning strategies that account for the interplay between US and foreign tax rules. Together, these three professionals form the core of your advisory team. Depending on your circumstances, you may also need specialists in areas such as retirement plan optimization, real estate taxation, or business succession planning.

Key Takeaways

The tax implications of the US Gold Card Visa program are substantial and far-reaching. As you evaluate whether this pathway to US permanent residency is right for you, keep the following essential points in mind.

- Gold Card holders are subject to worldwide income taxation. From the date you become a permanent resident through the Gold Card, the United States will tax your global income regardless of where it is earned or held. This is a fundamental shift that affects virtually every aspect of your financial life. Note: the Platinum Card ($5M, not yet available) has been discussed as potentially offering exemption from US tax on non-US-sourced income, but this does not apply to Gold Card holders.

- The Gold Card gift payment is non-deductible. The $1 million individual Gold Card gift payment (plus $15,000 processing fee), paid to the Department of Commerce after vetting, is not expected to produce any tax benefit, deduction, or recoverable loss. It should be treated as an after-tax cost in your financial planning.

- Pre-immigration planning is critical and time-sensitive. The window before you become a US tax resident is the most valuable planning period. Strategies such as step-up in basis, trust restructuring, and PFIC liquidation are most effective or only available during this window.

- Reporting obligations are extensive and penalties are severe. FBAR, FATCA, and various IRS information returns create a comprehensive reporting framework for foreign assets. Non-compliance can result in penalties of tens of thousands of dollars per form per year, even when no tax is owed.

- State selection significantly affects your tax burden. Your choice of state of residence can result in millions of dollars in additional or avoided state income tax over your lifetime. This decision should be made strategically as part of your overall plan.

- Estate and gift tax planning must begin immediately. With rates up to 40% on worldwide assets, estate tax planning is essential for high-net-worth Gold Card Visa holders, particularly given the scheduled reduction in the federal exemption amount.

- Professional guidance is non-negotiable. The complexity and stakes involved in the tax transition to US residency demand a qualified team of professionals, including an international tax attorney, a cross-border CPA, and a wealth advisor with international expertise. The cost of professional advice is a small investment compared to the cost of mistakes.

- Start planning early. Ideally, your tax planning should begin twelve to twenty-four months before you intend to establish US residency. This allows adequate time for asset valuation, restructuring, exit tax planning, and coordination between advisors in multiple jurisdictions.

The US Gold Card Visa program represents a significant opportunity for qualified applicants to obtain US permanent residency. However, the financial success of this decision depends heavily on the quality of your pre-immigration and ongoing tax planning. By engaging the right professionals early, understanding the scope of your obligations, and executing a comprehensive tax strategy, you can make this transition with confidence and clarity.

For a broader overview of the Gold Card Visa program, eligibility requirements, frequently asked questions, and how it compares to other immigration pathways, visit our complete Gold Card Visa guide.

Related: Gold Card vs O-1 Visa: Is Paying $1M Worth It?

📋 Free Download: The Complete Gold Card Visa Guide 2026

Get our comprehensive PDF guide — Gold Card vs EB-5, qualification checklist, attorney selection guide, and more.

No spam. Unsubscribe anytime.

Related: Trump Gold Card Lawsuit: Legal Challenges and Risks for Investors [2026 Updates]

Stay Updated on Gold Card Visa Changes

Get real-time updates on policy changes, processing times, and legal developments. Free newsletter, no spam.

About the Editorial Team

This article was researched and written by the editorial team at usgoldcardvisaprogram.com. We specialize in US immigration investment programs and provide well-researched, regularly updated content. Our information is sourced from official government publications, immigration law firms, and verified policy documents. This content does not constitute legal or financial advice.

Need Help Finding the Right Immigration Attorney?

The Gold Card requires specialized legal expertise. We've put together a guide on what to look for.

Find a Gold Card Attorney →